Request Your Custom Analysis

Does Missing the Best Market Days Really Destroy Returns?

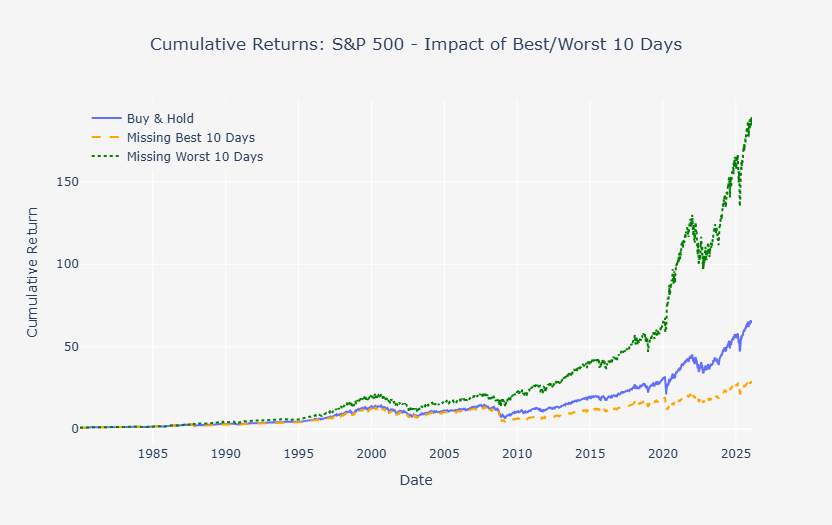

What really happens if you miss the “10 best market days”?

This popular investment claim is repeated everywhere — but rarely examined with real data. In this quantitative study, we analyse S&P 500 returns from 1980 to 2025, extract the actual best and worst days in the market, and compare three strategies: buy‑and‑hold, missing the best days, and avoiding the worst days. The results reveal a surprising truth: extreme up‑ and down‑moves cluster together, making market timing far harder than it seems. This research cuts through the myth with hard numbers, clear visualizations, and data‑driven insights for long‑term investors.

Get in Touch

Do you have a specific ticker on your watchlist that requires a deeper look? Whether it’s an individual stock, a commodity, or a niche index, I can apply the Cephu Multi-Lens Methodology to your request.

Simply fill out the form. I prioritize requests from our active community members and supporters. Use this tool to cut through the noise with data-driven precision.